I'm talking about the investing markets, because we know that the market always cycles – typically every six to eight years. We go through an upswing, the topping of the market, then a downswing which is a correction and then back up again. This has happened over decades and decades, going back to the mid 1800s when we first were measuring market cycles.

This last one has been a relatively long stretch on the upside. We came out of the great financial recession back in 2008, where we really hit the bottom of it in 2010-2012. Since that point, it’s been a straight shot up in the financial markets, real estate, and every kind of asset you could think of. Why? The overriding cheap money.

For many years, the federal reserve has been able to subsidize low interest rates because we've had low inflation. Well, we're seeing a change in the markets right now. If you're awake at all, you know that we've seen a lot of volatility since the first of this year. It’s been all over the board. The financial markets always react first. These are the emotional markets, the markets that can go on a downside very, very quickly.

The real estate markets are not immune to the market cycles.

It's just a different asset class and it's much slower to make changes. Therefore, in my experience, it’s much easier to follow the big waves and not get caught in these emotional cycles of the financial markets.

That's why so many people have been looking at real estate over the last number of years, because of the stability. It gives long-term stability, if you do it right.

Now, here's where the danger comes in. The party's been great over the last 10 years, but there's always Johnny-come-latelys to every up market cycle in every asset class. There's always people who come in late to the game because everybody else has been doing it. They say, “Hey, I want to get in too.”

That continues to push the asset bubbles up higher and higher, as long as there's still margin left. Now with the federal reserve raising interest rates, fighting with the headwinds of inflation, the market cycle is tipping on the downside. We are there. It's still volatile, going up and down, but I believe we're going into a significant recession/correction.

What does that mean for us as investors? Particularly, if you want to be a passive investor, not boots on the ground and not managing a company's assets or real estate – how do you know where to plant your flag?

That's the danger. Most people look at real estate investing as owning the asset. Some type of ownership, either owning a rental property, or putting money into a syndication where someone else is running the operations of a multi-family facility, or a self storage or mobile home park community. But that’s putting money into the equity side of real estate.

That's where all the upside comes from – equity. Ownership. You get the benefits of profits and cash flows going up, plus tax deductions.

That’s great when we're in a growth cycle. But what about when we're going through a correction? How do you position yourself there? See, most of the Johnny-come-latelys just don't understand. They've never gone through different iterations of the models.

I've been investing in real estate since 1980 – that's over four decades. I’ve watched these iterations, and I've gone through my own market cycles. I've done it with Freedom Founders for just over a decade. It's exactly how we position ourselves to know if we should take the equity side (the ownership side) or the other side. “Well what’s that, David? I didn’t know there was another side.”

The other side is the debt side.

Not debt as a liability, as we normally think of debt where we owe the money to the bank or owe money to a lender. No, this is where we get to be the lender. Instead of taking the equity position, with all the upside, gains and what everybody likes in a frothy market – how about if we take a different position and be a lender?

“Well, how does that work, David? I thought people went to the banks to get their money.” Yes they do, but let me give a quick example of what I call…

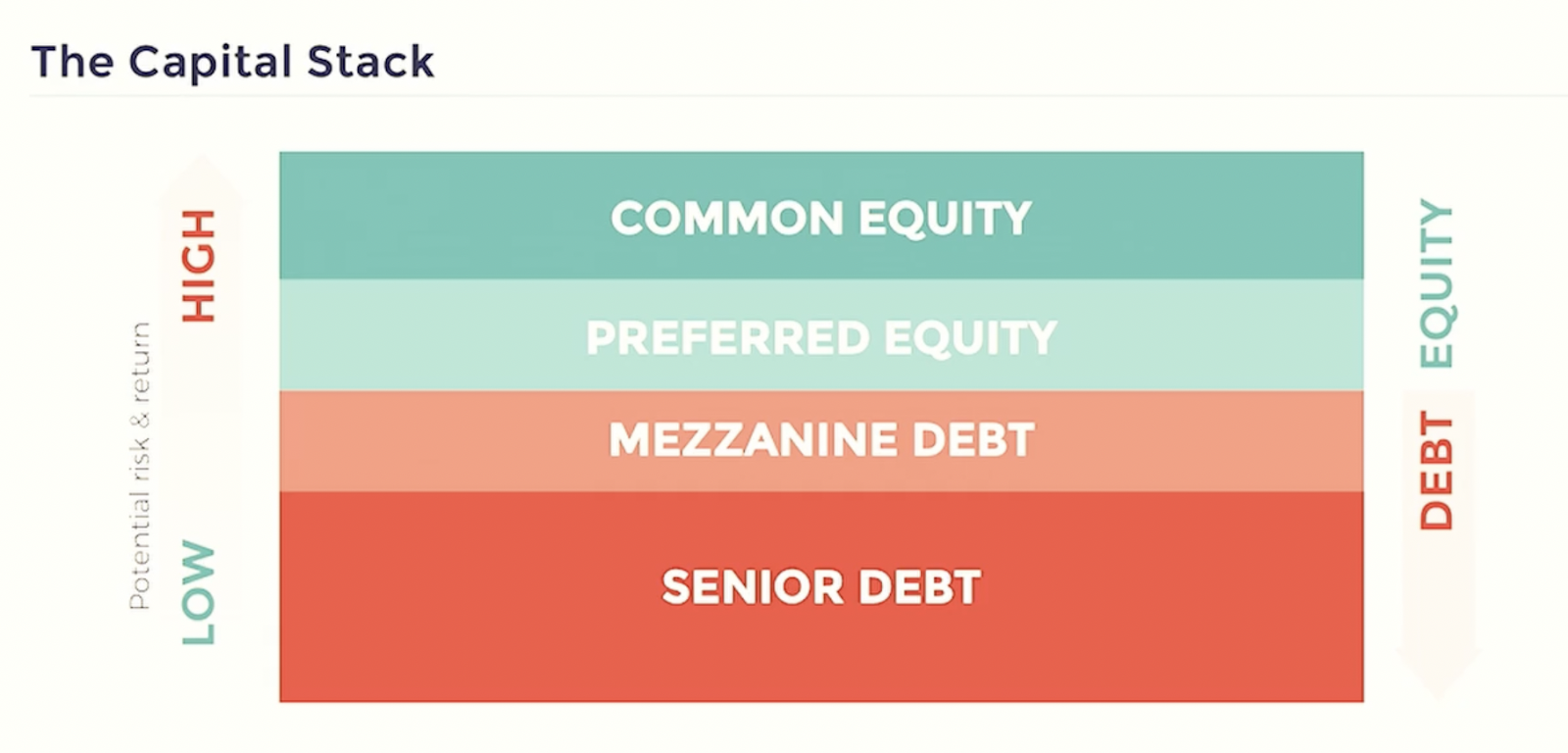

The Capital Stack

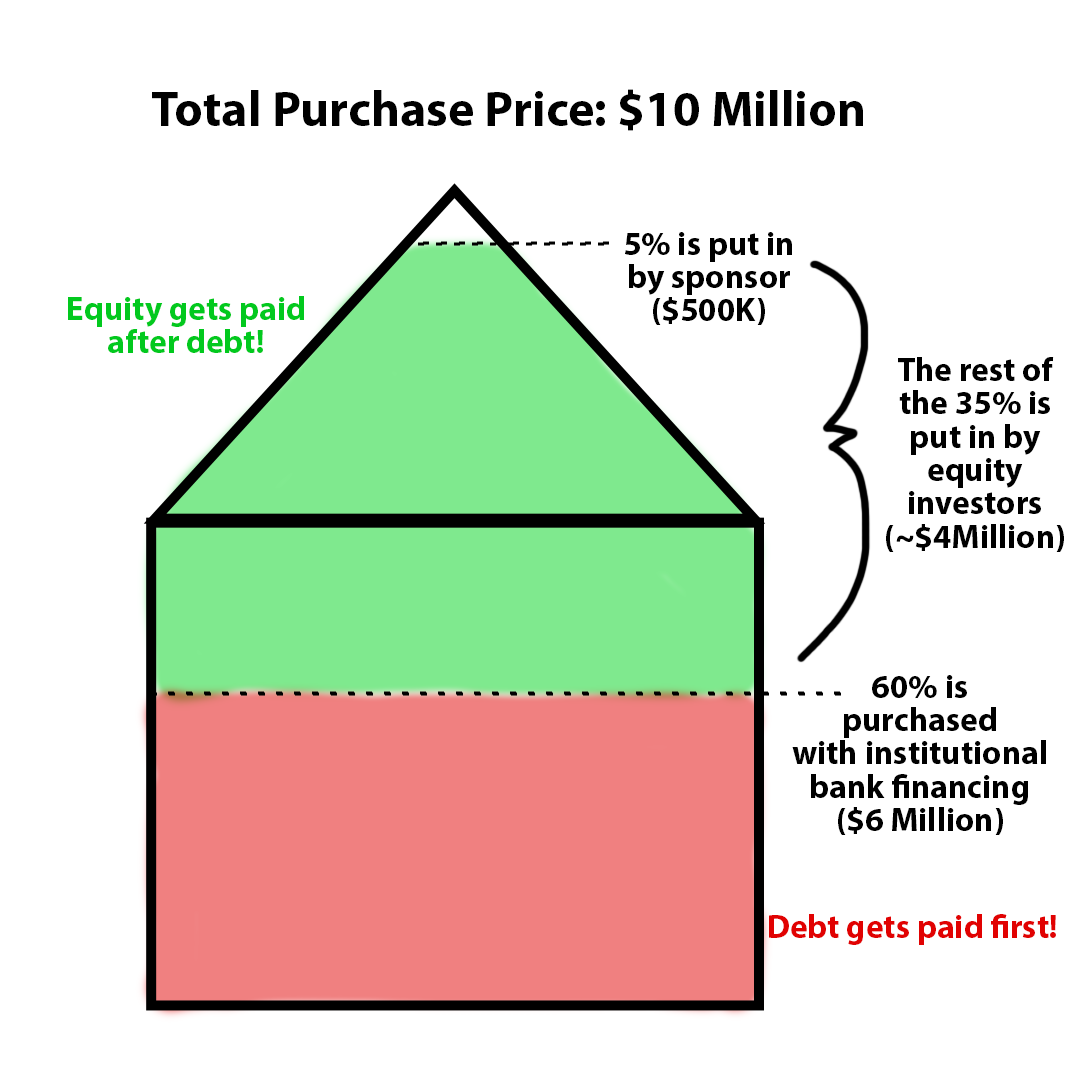

Imagine a simple diagram of a house composed of a square box and a triangle head. For the purpose of this example let's say it’s a multifamily apartment complex. And let’s say the purchase price of this opportunity for this complex is going to be a total of $10 million. That's the total purchase price.

There's a sponsor or a manager who makes a business out of finding these multi-family complexes and buys them at the best price with terms that work for them. So what do they do? They can usually get about 60% of the financing from a traditional bank institution. In this case, that would be $6 million. That means the rest of the 10 million has to be taken care of in another way. Where does that money come from?

The sponsor may put a little bit of money in and that's important. Maybe they put in 5%, which means $500,000. Then the rest of the capital, which is approximately $4 million, is going to come from equity investors.

Now, equity investors are always going to be paid second. Debt gets paid first. That's why I'm saying, right now, to be a debt lender. Sometimes in a market that’s going through corrections, it makes a lot more sense to be a debt lender.

You don't get all the tax benefits or upsides, but what if I just want to protect my capital and still get a decent return while we're going through a market cycle correction? Wouldn't that be higher ground?

For me, it is.

I take a lot of these debt positions right now because I want more safety. I will forgo the minimal potential that this market will keep going up and never stop, but the reality is, the markets will stop going up. There's always a time when market's shift and correct. And that means as a debt lender, I can lend my money and get paid first before the equity, as shown in my diagram below.

The equity ownership, in green, would be above the loan, the debt portion, which is in red. So if I want to play the game down here, I can get my returns and be secured by actually lending the money letting somebody else take that risk up here.

That's the difference in knowing how to slice and dice the current marketplace. I still invest in both equity and debt, but in Freedom Founders, we get the advantage of having the leverage of our entire community (having a lot of capital) which allows us to look at a lot of different opportunities. Our leverage position in the marketplace also allows us to structure where we want to be in the capital stack.

Would we want to take an equity position? How would that look? Would we take preferred equity? Common equity? What's the waterfall? This is a term that you may not be accustomed to, but we get to negotiate these things.

If we want to be on the debt lender side, can we have the debt position, the safer position while also having an equity play at the same time? Yes, it can be done. This is the advantage of knowing how the market cycles work, how to structure deals and having the leverage of a lot of capital.

You couldn’t do this as an individual passive investor,

because you pretty much have to just take what's given to you. If you want to invest in real estate and you're not going to do it yourself, you may be provided an opportunity to invest in this or that syndication (or other opportunity), but they've already got it exactly laid out where you're going to be in the capital stack.

Is that where you want to be in this market cycle right now, when we're going through a correction phase? I would say not. Don't be a Johnny-come-lately that does not have a position that allows you to be safe and profitable in this market. If not through your own experience, you need to find the right people to get you through it.

When should you turn back to more equities and more of an aggressive position? Well, after we've gone through a market cycle, assets go on sale. Do you have that positioning? Do you know who to call on? Do you have different asset class diversification? Geographic diversification? These are all the advantages of real estate, a very inefficient market, but you've got to have the relationships and the access points. That’s exactly what we do in Freedom Founders.

If you don’t have those, you've got to be very careful right now as an investor, especially if you’re a Johnny-come-lately. If this is new to you, this is a time to proceed with extreme caution.